- Properties of the parabolic partial differential equation

- the meaning of terms in the Black-Scholes equation

Putting the Black-Scholes equation into historical perspective

The Black-Scholes partial differential equation is in two dimensions, S and t. It is a parabolic equation, meaning that it has a second derivative with respect to S, and a first derivative with respect to t. Equations of this form are more colloquially known as heat or diffusion equations.

The meaning of the terms in the Black-Scholes equation

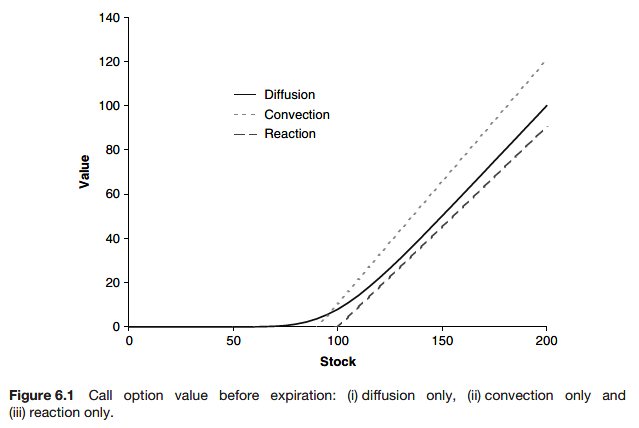

The Black-Scholes equation can be accurately interpreted as a reaction-convection-diffusion equation.

\[ \frac{\partial V}{\partial t} + \frac{1}{2}\sigma^2 S^2 \frac{\partial^2 V}{\partial S^2} \]

If these were the only terms in the Black-Scholes equation it would still exhibit the smoothing-out effect, that any discontinuities in the payoff would be instantly diffused away. The only difference between these terms and the terms as they appear in the basic heat or diffusion equation, is that the diffusion coefficient is a function of S. Thus we really have diffusion in a nonhomogeneous medium.

The first-order S-derivative term

\[ r S \frac{\partial V}{\partial S} \]

can be thought of as a convection term. If this equation represented some physical system, then the convective term would be due to a breeze, blowing the smoke in a preferred direction.

The final term

\[ -rV \]

is a reaction term. Balancing this term and the time derivative would give a model to decay of a radioactive body, with the half-life being related to r.

Putting these terms together we get a reaction-convection-diffusion equation. An almost identical equation would be arrived at for the dispersion of pollutant along a flowing river with absorption by the sand. In this, the dispersion is the diffusion, the flow is the convection, and the absorption is the reaction.

Convection-diffusion equation

The convection–diffusion equation is a combination of the diffusion and convection (advection) equations, and describes physical phenomena where particles, energy, or other physical quantities are transferred inside a physical system due to two processes: diffusion and convection.

\[ \frac{\partial c}{\partial t} = \triangledown \cdot (D \triangledown c) - \triangledown \cdot (vc) + R \]

where

- c is the variable of interest (species concentration for mass transfer, temperature for heat transfer)

- D is the diffusivity (also called diffusion coefficient), such as mass diffusivity for particle motion or thermal diffusivity for heat transport

- v is the velocity field that the quantity is moving with. It is a function of time and space. For multiphase flows and flows in porous media, v is the (hypothetical) superficial velocity.

- R describes sources or sinks of the quantity c. For example, for a chemical species, R > 0 means that a chemical reaction is creating more of the species, and R < 0 means that a chemical reaction is destroying the species. For heat transport, R > 0 might occur if thermal energy is being generated by friction.

- ∇ represents gradient and ∇ ⋅ represents divergence. In this equation, ∇c represents concentration gradient.

Convection

Convection is single or multiphase fluid flow that occurs spontaneously due to the combined effects of material property heterogeneity and body forces on a fluid, most commonly density and gravity (see buoyancy).

Diffusion

Diffusion is the net movement of anything (for example, atoms, ions, molecules, energy) generally from a region of higher concentration to a region of lower concentration

Boundary and initial/final conditions

Boundary conditions tell us how the solution must behave for all time at certain values of the assets. In financial problems we usually specify the behavior of the solution at S = 0 and as \(S \to \infty\). We must also tell the problem how the solution begins. The Black-Scholes equation is a backward equation, meaning that the signs of the t derivative and the second S derivative in the equation are the same when written on the same side of the equals sign. We therefore have to impose a final condition. This is usually the payoff function at expiry.

The Black-Scholes equation in its basic form is linear and homogeneous, and therefore satisfies the superposition principle; add together two solutions of the equation and you will get a third. Another nice property is the uniqueness of the solution. Provided that the solution is not allowed to grow too fast as S tends to infinity the solution will be unique.

Quantum Superposition

Quantum superposition is a fundamental principle of quantum mechanics that states that linear combinations of solutions to the Schrödinger equation are also solutions of the Schrödinger equation. This follows from the fact that the Schrödinger equation is a linear differential equation in time and position. More precisely, the state of a system is given by a linear combination of all the eigenfunctions of the Schrödinger equation governing that system

Some solution methods

Transformation to constant coefficient diffusion equation

\[ V(S, t) = e^{\alpha x + \beta \tau}U(x, \tau) \]

where

\[ \alpha = -\frac{1}{2}(\frac{2r}{\sigma^2} - 1), ~ \beta = -\frac{1}{4} (\frac{2r}{\sigma^2} + 1)^2, ~ S = e^x ~ and ~ t = T - \frac{2\tau}{\sigma^2} \]

then \(U(x, \tau)\) satisfies the basic diffusion equation

\[ \frac{\partial u}{\partial \tau} = \frac{\partial^2 u}{\partial x^2} \]

One solution of the Black-Scholes equation is

\[ V'(S, t) = \frac{e^{-r(T - t)}}{\sigma S' \sqrt{2\pi(T - t)}}e^{-(\log{(S / S')} + (r - \frac{1}{2}\sigma^2(T - t))^2 / 2\sigma^2 (T - t)} \]

for any S’. This solution is special because t → T it becomes zero everywhere, except at S = S’. In this limit the function becomes what is known as a Dirac delta function. Think of this as a function that is zero everywhere except at one point where it is infinite, in such a way that its integral is one.

The equation is a solution of the Black-Scholes equation for any S’. Because of the superposition principle we can multiply by any constant, and we get another solution. But then we can also get another solution by adding together expressions of the equation but with different values for S’. Putting this together, and thinking of an integral as just a way of adding together many solutions, we find that

\[ \frac{e^{-r(T - t)}}{\sigma S' \sqrt{2\pi(T - t)}}\int_0^\infty{e^{-(\log{(S / S')} + (r - \frac{1}{2}\sigma^2(T - t))^2 / 2\sigma^2 (T - t)}f(S')\frac{dS'}{S'}} \]

is also a solution of the Black-Scholes equation for any function of f(S’).

Because of the nature of the integrand as t → T, if we choose the arbitrary function f(S’) to be the payoff function then this expression becomes the solution of the problem:

\[ V(S, t) = \frac{e^{-r(T - t)}}{\sigma S' \sqrt{2\pi(T - t)}}\int_0^\infty{e^{-(\log{(S / S')} + (r - \frac{1}{2}\sigma^2(T - t))^2 / 2\sigma^2 (T - t)}f(S')\frac{dS'}{S'}} \]

The function V’(S, t) is the Green’s function.

어떤 기초자산과 거기에 연동된 옵션의 payoff가 어떤 함수의 형태를 가지고 있던, Black-Scholes equation으로 계산 가능.

Series solution

Sometimes we have boundary conditions at two finite (and non-zero) values of S, \(S_u\) and \(S_d\). For this type of problem, we postulate that the required solution of the Black-Scholes equation can be written as an intinite sum of special functions. First of all, transforms to the nicer basic diffusion equation in x and \(\tau\).

\[ e^{\alpha x + \beta \tau}\sum_{i = 0}^\infty{a_i(\tau)\sin{(i\omega x)} + b_i(\tau)\cos{(i\omega x)}} \]

for some \(\omega\) and some functions a and b to be found. The linearlity if the equation suggests that a sum of solutions might be appropriate. If this is to satisfy the Black-Scholes equation then we must have

\[ \frac{da_i}{d\tau} = - i^2 \omega^2 a_i(\tau) ~ and ~ \frac{db_i}{d\tau} = -i^2 \omega^2 b_i(\tau) \]

You can easily show this by substitution. The solutions are thus

\[ a_i(\tau) = A_ie^{-i^2 \omega^2 \tau} ~ and ~ b_i(\tau) = B_ie^{-i^2 \omega^2 \tau} \]

The solution of the Black-Scholes equation is therefore

\[ e^{\alpha x + \beta \tau}\sum_{i = 0}^\infty{e^{-i^2 \omega^2 \tau}\sum_{i = 0}^\infty{A_i\sin{(i\omega x)} + B_i\cos{(i\omega x)}}} \]

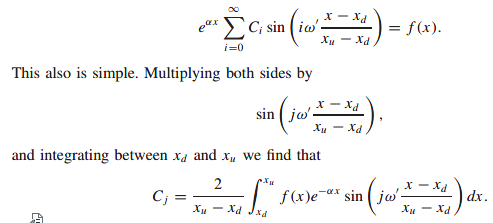

Consider the example where the payoff at time \(\tau = 0\) is f(x), but the contract becomes worthless if every \(x = x_d\) or \(x = x_u\)

Rewrite the term as

To ensure that the option is worthless on these two x values, choose \(D_i = 0\) and \(\omega' = \pi\). The boundary conditions are thereby satisfied. All that remains is to choose the \(C_i\) to satisfy the final condition:

This technique, which can be generalized, is the Fourier series method. There are some problems with the method if you are trying to represent a discontinuous function with a sum of trigonometrical functions. The oscillator nature of an approximate solution with a finite number of terms is known as Gibbs phenomenon.

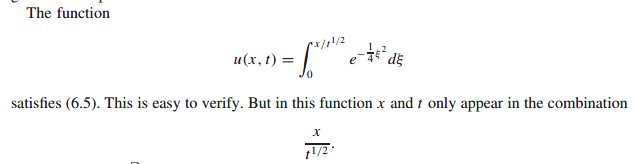

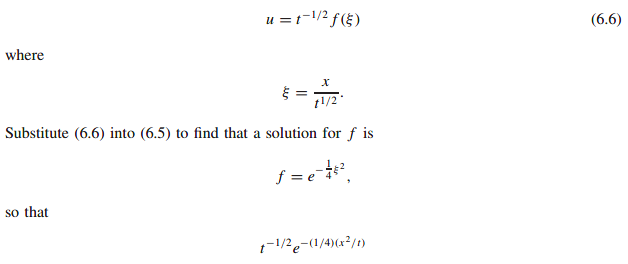

Similarity reductions

\[ \frac{\partial u}{\partial t} = \frac{\partial^2 u}{\partial x^2} \]

This basic diffusion equation is an equation for the function u which depends on x and t. Sometimes, in very, very special cases, there is the solution as a function of just one variable.

A slight generalization, but also demonstrating the idea of similarity solutions, is to look for a solution of the form

is also a special solution for the diffusion equation.

Yu can’t always find similarity solutions; not only must the equation have a particular nice structure but also the similarity form must be consistent with any initial condition or boundary conditions.

Other analytical techniques

Fourier and Laplace transforms

Recently these techniques have become useful in some higher dimensional models such as those incorporating stochastic volatility.

Numerical solution

In the vast majority of cases we must solve the Black-Scholes equation numerically. Parabolic differential equations are just about the easiest

Further reading