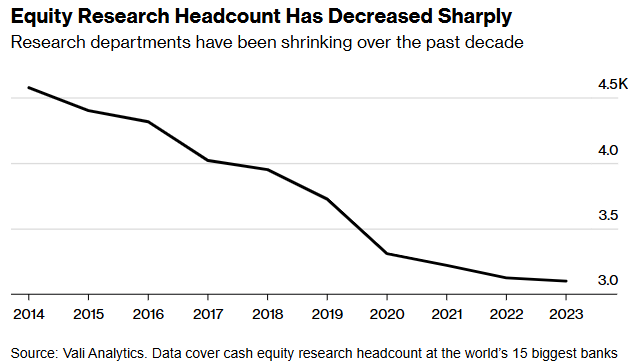

Few corners of finance have been hit harder by job cuts in recent years than equity research. Regulations on how banks charge for research, a shrinking market for publicly listed companies, and the popularity of index-tracking funds have conspired to squeeze equity research in ways few could have imagined even a decade ago. Leaps in artificial intelligence only threaten to accelerate that trend, with firms like JPMorgan already experimenting with AI-powered analyst chatbots, sowing deeper doubts about the value of fundamental analysis and whether investors will keep paying for it.

The fallout is already reshaping Wall Street. But it’s also having knock-on effects on the structure of the stock market itself, in how individual companies, both big and small, are valued.

지난 몇 년간 금융권에서 구조조정의 타격을 가장 크게 받은 분야는 주식 리서치입니다. 리서치 수수료에 대한 규제, 상장기업 시장의 축소, 그리고 인덱스 펀드의 인기로 인해 10년 전만 해도 상상하기 힘들 정도로 주식 리서치가 위축되었습니다. 인공지능의 발전은 이러한 추세를 더욱 가속화할 것으로 보이는데, JP모건과 같은 기업들이 이미 AI 기반 애널리스트 챗봇을 실험하면서 기본적 분석의 가치와 투자자들의 지속적인 비용 지불 의사에 대한 의구심이 더욱 깊어지고 있습니다.

이러한 여파로 월스트리트가 이미 재편되고 있습니다. 더불어 대기업과 중소기업을 막론하고 개별 기업의 가치 평가 방식 등 주식시장의 구조 자체에도 연쇄적인 영향을 미치고 있습니다.

Meanwhile, despite a small uptick in the first half of last year, spending on research globally has sunk 50% since 2018, data from Substantive Research show. That year, MiFID II was enacted, forcing asset managers in the UK and European Union to pay for research, rather than offering it for free as part of a suite of services.

한편, 작년 상반기에 소폭 상승했음에도 불구하고, Substantive Research의 데이터에 따르면 글로벌 리서치 지출이 2018년 이후 50% 감소했습니다. 2018년에는 MiFID II가 시행되어 영국과 유럽연합의 자산운용사들이 서비스 패키지의 일부로 무료로 제공하던 리서치를 별도로 구매해야 하게 되었습니다.

Hard dollar는 일반적으로 물건을 주고, 물건의 대가를 받는 관행이라고 보면 되고, soft dollar는 물건에 대가가 명확하지 않은 일부 서비스를 추가해주면서 물건의 대가만 받는 관행이라고 보면 된다.

Buy side에 돈을 맡긴 client, client의 돈을 운용하는 buy side, brokerage를 제공하는 sell side, 3자 사이에서 client의 이익이 침해될 수 있는 conflict of interest (이해상충)을 방지하고자 유럽에서 research material에 hard dollar 관행을 적용하라는 규칙으로 인해 생긴 일이다.

Buy side는 client의 돈을 받아 sell side의 brokerage service를 활용하여 transaction execution을 통해 운용한다. 이 과정에서 sell side는 고객 유치를 위해 brokerage service를 제공하면서 받는 brokerage fee에 research material이나 부가 서비스를 붙여서 제공하게 되고 이런 서비스의 대가를 soft dollar라고 부른다. buy side는 더 나은 운용을 하기 위해 이런 서비스를 마다하지 않게 되는데, 이 과정에서 buy side가 client의 돈으로 sell side에게 brokerage fee를 과하게 줄 여지가 생기게 된다. 이를 방지하고자 유럽에서는 아예 research material에도 hard dollar 관행을 적용하는 법을 제정한 것이고, 미국은 아직 soft dollar 관행을 유지하고 있다.

Europe의 research analyst는 research material에 대한 hard dollar 관행 덕분에 조금 살아남고 있다는 게 기사의 이야기.

The buyside is feeling the pinch, too. Matt Stucky, a money manager at Northwestern Mutual Wealth Management, says there either simply aren’t enough analysts covering the companies he’s interested in or they’re spread too thin. As a result, he’s had to do more of the legwork himself to get the answers he wants.

You don’t get the “same level of information you had when a company had 20 people covering it,” Stucky said.

Currently, companies in the Russell 2000 Index with fewer than 10 analyst recommendations have ballooned to some 1,500 from 880 a decade ago, an increase of 70%, data compiled by Bloomberg show. Conversely, coverage has become concentrated in the biggest names. Today, about 97% of the S&P 500 have 10 or more ratings, up from about two-thirds in 2014.

A growing body of evidence suggests stocks that fall off the sell-side radar often struggle to attract investors, distorting valuations and making markets less efficient.

One academic paper, which looked at data over a 40-year period, showed how investors consistently over- or undervalued companies covered by fewer analysts. Another study found firms that had a decrease in coverage showed a significant decline in investor recognition, increasing their cost of capital. A third showed that low-coverage stocks traded less and had wider bid-ask spreads, while “orphaned” companies were far more likely to be delisted.

They’re also more likely to underperform. Small-cap companies with no coverage, for example, have lagged behind those covered by more than 10 analysts by nearly 3 percentage points a year since 2001, according to Steven DeSanctis, a small- and mid-cap strategist at Jefferies.

“For small companies that are already covered by fewer analysts to start with, each one less will hurt them more,” said Kevin Li, a professor at Santa Clara University and co-author of one of the papers. “The downtrend is probably not preventable, given the move away from active investment. Now, with AI, we could see that (human) role reduce further.”

매수 측도 압박을 느끼고 있습니다. Northwestern Mutual Wealth Management의 자금 운용사 Matt Stucky는 관심 있는 기업들을 커버하는 애널리스트가 충분하지 않거나 너무 얇게 분산되어 있다고 말합니다. 결과적으로 그는 원하는 답을 얻기 위해 더 많은 실사 작업을 직접 해야 했습니다.

“한 기업을 20명이 커버하던 시절과 같은 수준의 정보를 얻을 수 없습니다”라고 Stucky는 말했습니다.

블룸버그가 집계한 데이터에 따르면, 현재 Russell 2000 지수에서 애널리스트 추천이 10개 미만인 기업의 수가 10년 전 880개에서 1,500개로 70% 급증했습니다. 반대로 커버리지는 대형주에 집중되었습니다. 현재 S&P 500 기업의 약 97%가 10개 이상의 투자의견을 받고 있는데, 이는 2014년 약 3분의 2에서 증가한 수치입니다.

증가하는 연구 결과에 따르면 매도 측의 관심에서 벗어난 주식들은 투자자들의 관심을 끌기 어려워져 가치 평가가 왜곡되고 시장의 효율성이 저하되는 것으로 나타났습니다.

40년간의 데이터를 분석한 한 학술 논문은 투자자들이 애널리스트 커버리지가 적은 기업들의 가치를 지속적으로 과대 또는 과소평가하는 것을 보여줬습니다. 다른 연구에서는 커버리지가 감소한 기업들의 투자자 인지도가 크게 하락하여 자본비용이 증가하는 것으로 나타났습니다. 세 번째 연구는 커버리지가 낮은 주식들의 거래량이 적고 매수-매도 스프레드가 더 넓으며, ‘고아’ 기업들은 상장폐지될 가능성이 훨씬 높다는 것을 보여줬습니다.

이들은 또한 저조한 성과를 보일 가능성이 더 높습니다. Jefferies의 소형주 및 중형주 전략가 Steven DeSanctis에 따르면, 예를 들어 커버리지가 없는 소형주들은 2001년 이후 10명 이상의 애널리스트가 커버하는 기업들에 비해 연간 약 3%포인트 낮은 수익률을 기록했습니다.

“처음부터 적은 수의 애널리스트가 커버하는 소형 기업들의 경우, 애널리스트가 한 명씩 줄어들 때마다 더 큰 타격을 받게 될 것입니다”라고 Santa Clara University의 Kevin Li 교수이자 해당 논문들 중 하나의 공동 저자는 말했습니다. “액티브 투자에서 멀어지는 추세를 고려할 때 이러한 하락세는 막을 수 없을 것 같습니다. 이제 AI와 함께, 우리는 (인간의) 역할이 더욱 축소되는 것을 보게 될 수 있습니다.”

모두가 주목하는 주식만 cover하는 세상이 되서, 아마 가치투자나 small-mid cap은 fundamental research가 더 빛을 발할 수 있을 것 같다. 시장에 mispricing opportunity도 많을 것으로 보인다.

Part of the irony is that the lack of in-depth analysis which asset managers bemoan is a direct consequence of their unwillingness to pay for it. And as they “continue to spend less and less” for bank research, Integrity Research’s Mike Mayhew says they’ll likely look for more cost-effective ways to fill the gaps.

That includes relying on in-house analysts or non-bank sources like those on blogging platform Substack, often written by the very analysts caught up in budget cuts and staffing culls. Northwestern Mutual’s Stucky subscribes to a few himself and values their “unfiltered” takes. (He declined to identify them.)

Indeed, online finance blogs have exploded in recent years, with Substack estimating it now hosts tens of thousands of them.

Asked why they should stick with him rather than buying an ETF, Morris says history suggests the S&P 500’s outsize gains won’t likely last. Part of his draw, he says, is that he talks about his winners and losers and puts all his investable assets behind his calls.

“The industry has had issues in the past in terms of what the person writing the research actually thinks, versus what they would do if they were managing their own money,” he said.

자산운용사들이 한탄하는 심층 분석의 부재는 아이러니하게도 그들이 이에 대한 비용을 지불하지 않으려는 태도의 직접적인 결과입니다. Integrity Research의 Mike Mayhew는 자산운용사들이 “은행 리서치에 점점 더 적은 비용을 지출함에 따라” 격차를 메우기 위한 더 비용 효율적인 방법을 찾을 것이라고 말합니다.

여기에는 사내 애널리스트나 Substack과 같은 블로깅 플랫폼의 비은행권 정보원을 활용하는 것이 포함되며, 이러한 콘텐츠는 종종 예산 삭감과 인력 감축으로 인해 일자리를 잃은 바로 그 애널리스트들이 작성합니다. Northwestern Mutual의 Stucky도 몇 개의 구독권을 가지고 있으며 그들의 “필터링되지 않은” 견해를 높이 평가합니다. (그는 구체적인 대상은 밝히지 않았습니다.)

실제로 온라인 금융 블로그는 최근 몇 년간 폭발적으로 증가했으며, Substack은 현재 수만 개의 블로그를 호스팅하고 있다고 추산합니다.

ETF를 구매하는 대신 자신을 선택해야 하는 이유를 묻자, Morris는 역사적으로 볼 때 S&P 500의 큰 수익률이 계속되지는 않을 것이라고 말합니다. 그는 자신의 매력적인 점이 성공과 실패 사례를 모두 공유하고 자신의 투자 가능한 자산을 전부 자신의 투자 판단에 걸고 있다는 것이라고 말합니다.

“업계는 과거부터 리서치를 작성하는 사람이 실제로 생각하는 바와, 그들이 자신의 돈을 운용한다면 실제로 어떻게 할 것인지 사이에 괴리가 있었습니다”라고 그는 말했습니다.

AI와 passive investing trend로 인해 일자리를 잃은 analyst들의 이야기. 이들은 content creator가 되서 research material로 돈을 벌고 직접 운용까지 하고 있다. 여기에 자신의 일자리를 위협한 AI를 활용한 생산성 향상은 덤이다. Valuation challenge를 비롯한 가치있는 fundamental research가 sell side-buy side 간에만 주고받던 관계를 떠나 좀 더 자유로운 이해관계 아래서 꽃을 피운다고 봐도 될지도.

내 직업과 관련되어 있기도 하고, 사업적으로도 기록할만한 기사라서 따로 포스팅.