Financials

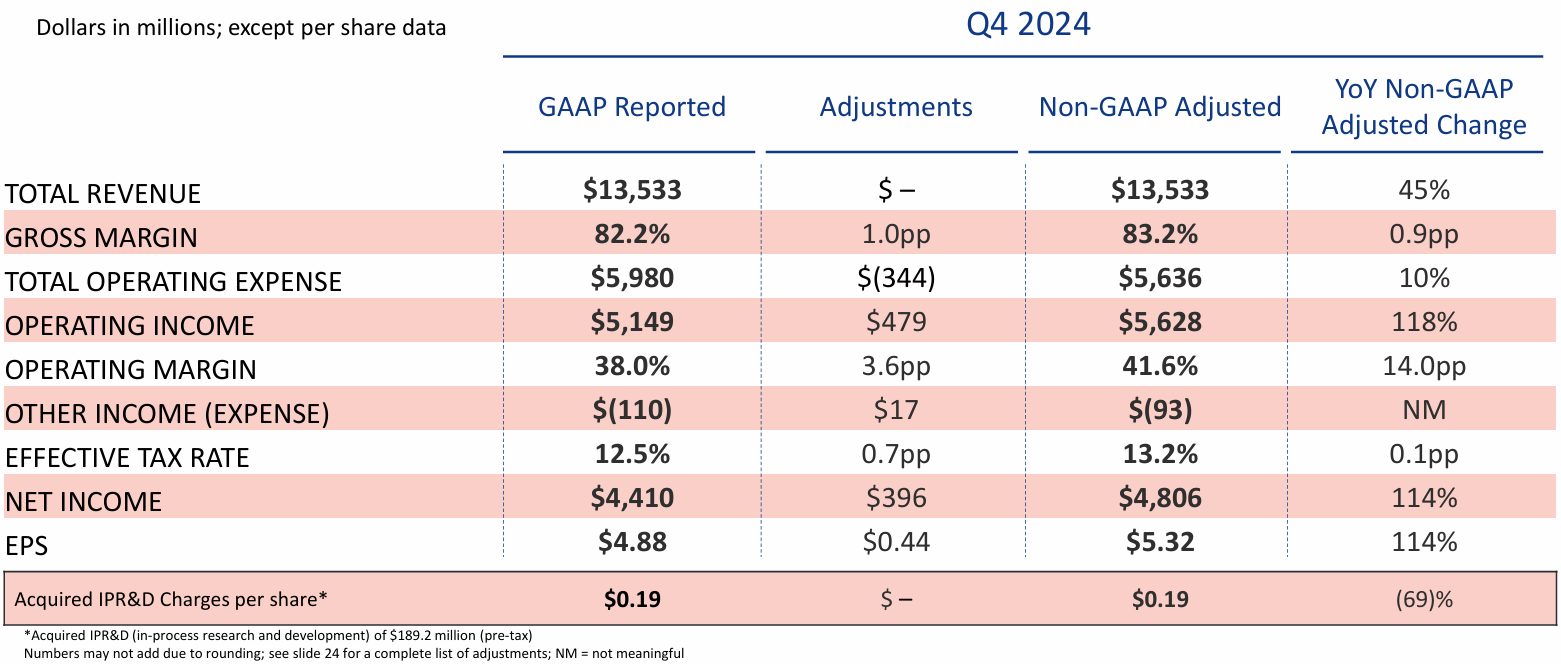

4Q24

Revenue grew 45%, driven by Mounjaro and Zepbound, while non-incretins grew 20%, , excluding onetime payments related to business development

4Q24 earnings (Source: Eli Lilly)

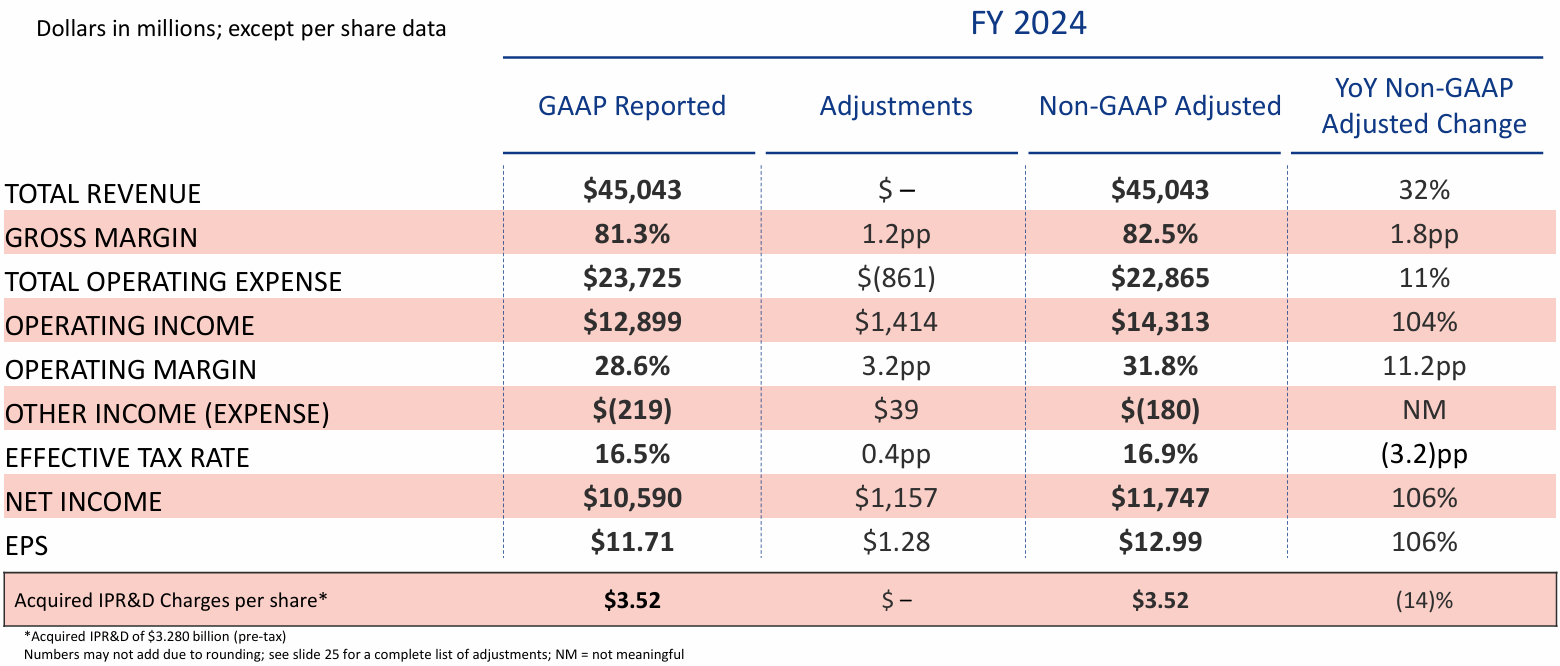

FY2024

Revenue: $45,043, yoy +32%, guidance/consensus miss

EPS: guidance miss, consensus beat

2024 earnings (Source: Eli Lilly)

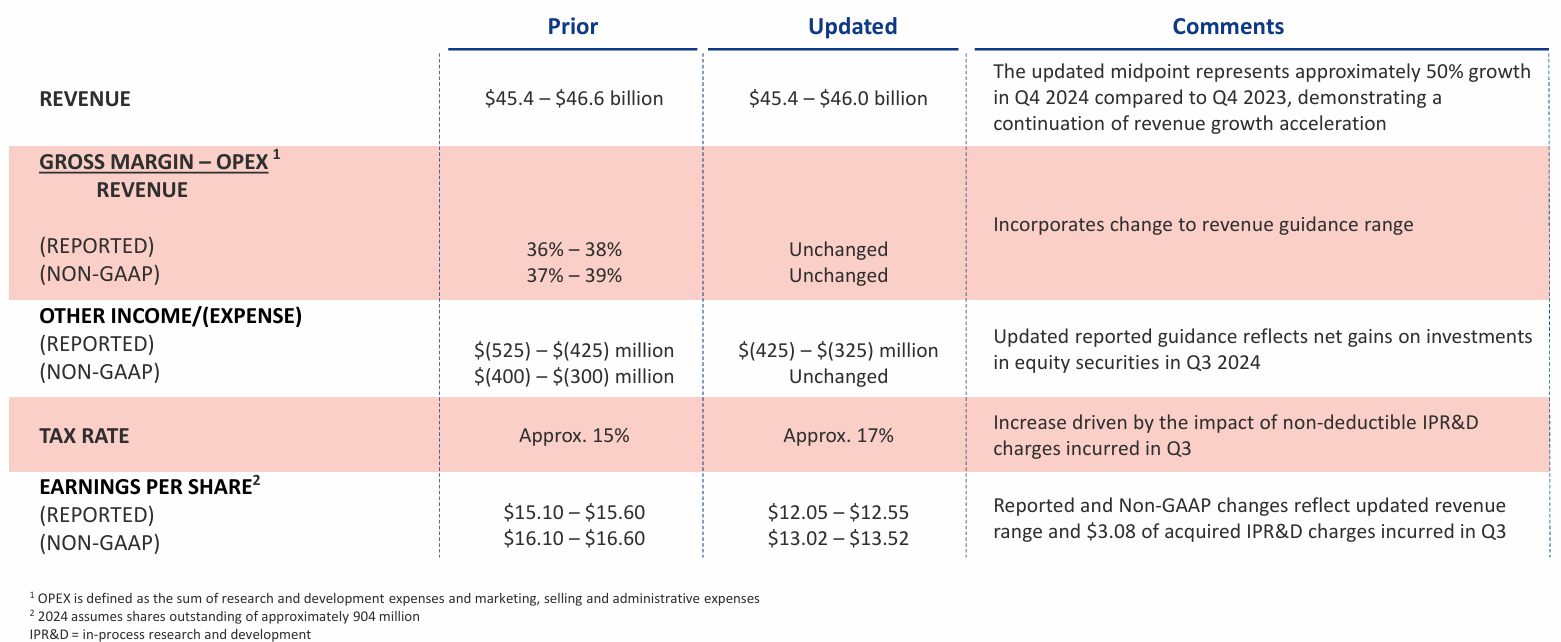

- 2024 guidance in 3Q24 (Source: Eli Lilly)

Guidance 하단까지 miss

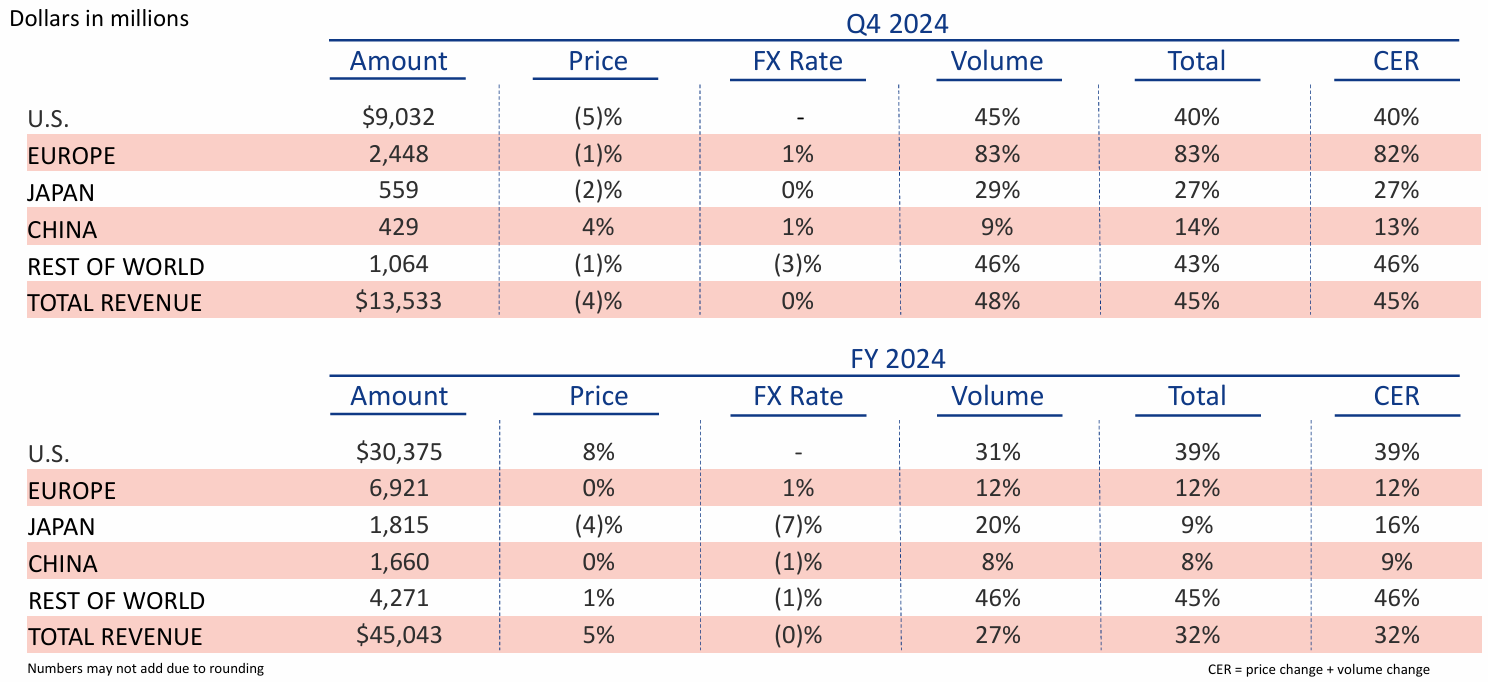

Price/volume breakdown (Source: Eli Lilly)

- 이 도표에서 US price -5%가 사실상 핵심

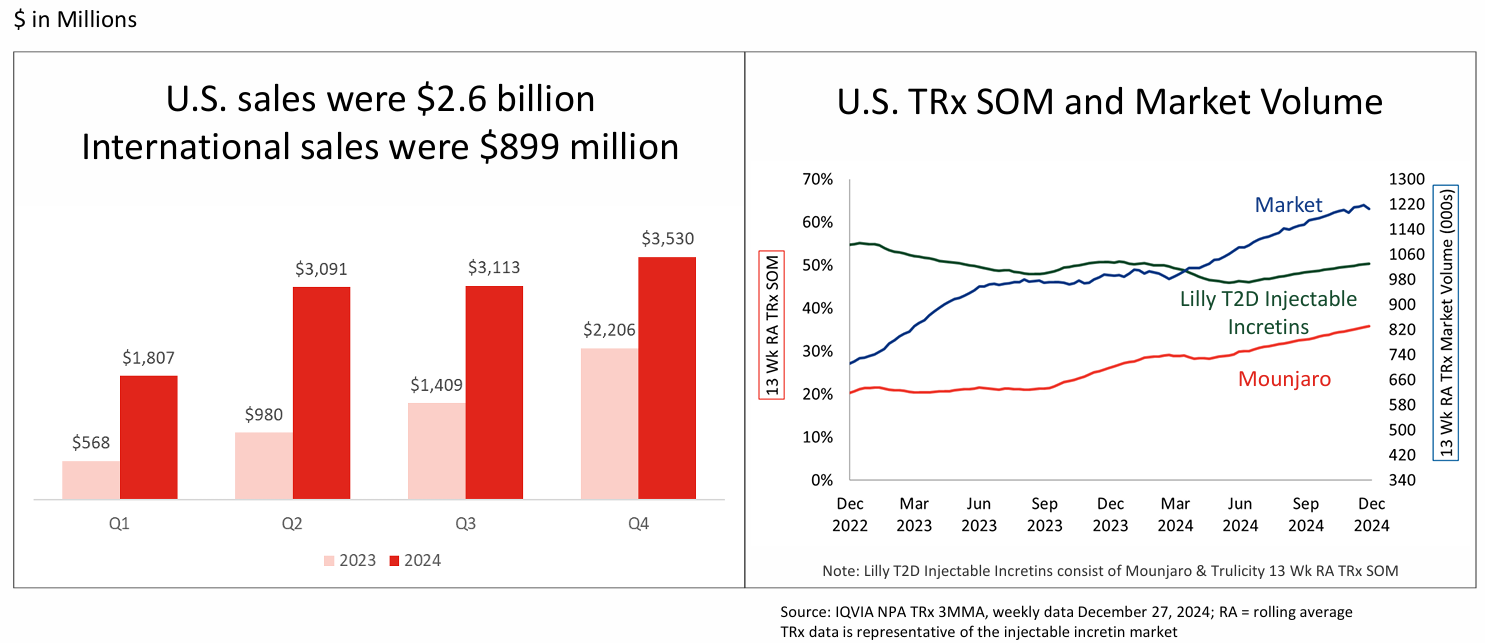

Zepbound and Mounjaro were again the largest growth contributors, partially offset by declines in Trulicity. Realized prices decreased 5% in the U.S. due to favorable changes to estimate for rebates and discounts related to Mounjaro in Q4 2023

Zepbound와 Mounjaro가 다시 한 번 가장 큰 성장 동력이었으며, 이는 Trulicity의 감소로 일부 상쇄되었습니다. 미국 내 실현 가격은 2023년 4분기 Mounjaro 관련 리베이트 및 할인 예상치의 유리한 변동으로 인해 5% 하락했습니다

- 4Q24 earnings call (Source: Eli Lilly)

- 3Q24 earnings call에서 favorable pricing이라는 단어를 봤을 때는 회사가 가격을 자신들에게 우호적으로 책정할 만큼 pricing power가 있구나, demand가 세구나 했는데…

- favorable price가 회사에 우호적인게 아니라 고객한테 우호적인거였네

Business

At the portfolio level, we anticipate foreign exchange to be a headwind as the dollar has strengthened relative to other currencies. In addition, we forecast overall net prices to decline by mid- to high single digits in percentage terms, including U.S. Part D changes.

포트폴리오 차원에서, 달러가 다른 통화 대비 강세를 보임에 따라 환율이 불리하게 작용할 것으로 예상됩니다. 또한, 미국 파트 D 변경사항을 포함하여 전체 순가격이 중반에서 후반대 한 자릿수 퍼센트 하락할 것으로 전망합니다.

- 4Q24 earnings call (Source: Eli Lilly)

- 내년에 또 가격 내려갈거라고

We had no wholesaler back orders as we closed 2024, and wholesalers have been fulfilling orders from pharmacies at very high levels.

2024년을 마감할 때 도매상의 미처리 주문이 없었으며, 도매상들은 매우 높은 수준으로 약국의 주문을 처리하고 있습니다.

- 4Q24 earnings call (Source: Eli Lilly)

Wholesaler에 대한 comment도 tone이 좀 바꼈다고 느꼈는데

연중 내내 부족하다 많이 가져간다 어쩐다 하더니 이번에는 약국 주문을 처리하는데 문제가 없다고 하십니다

여기서 분위기가 예전에 비만약이 세상을 바꾸니 어쩌니하는 상황이랑 많이 다르다고 생각함

Mounjaro revenue and prescription trends (Source: Eli Lilly)

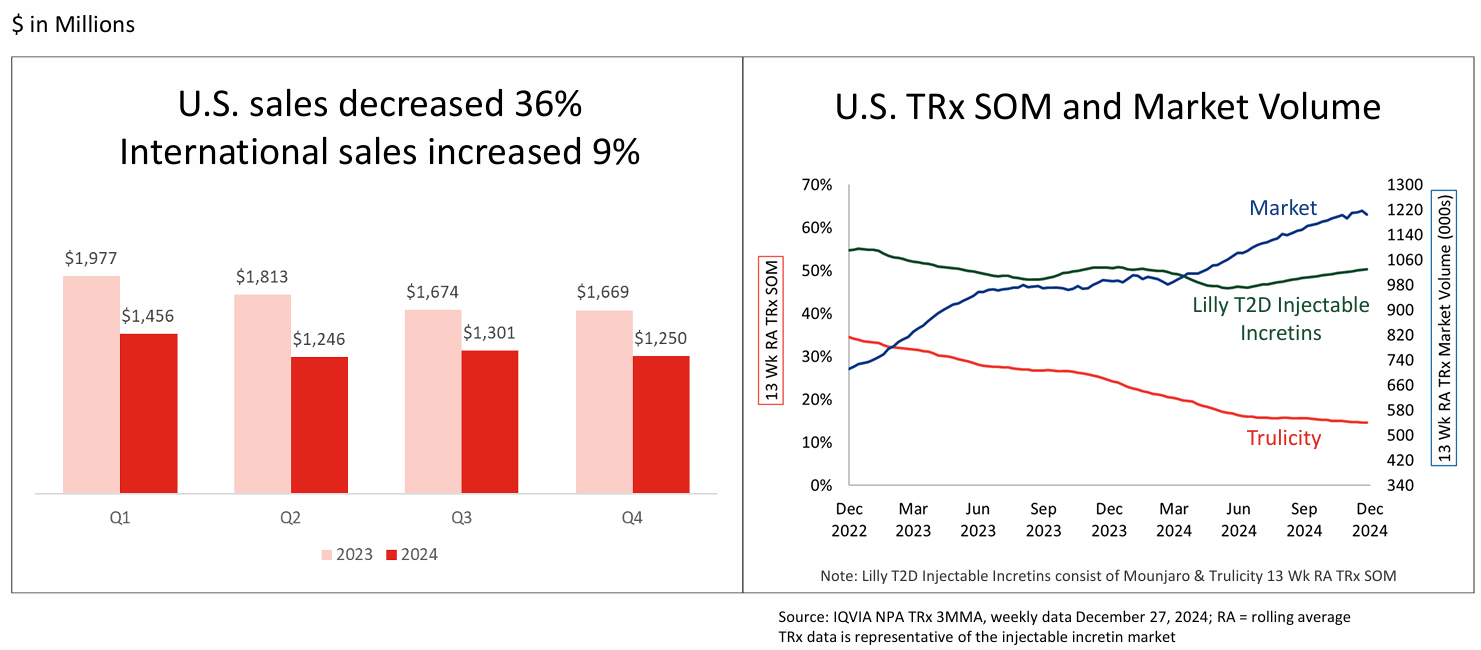

- Trulicity revenue and prescription trends (Source: Eli Lilly)

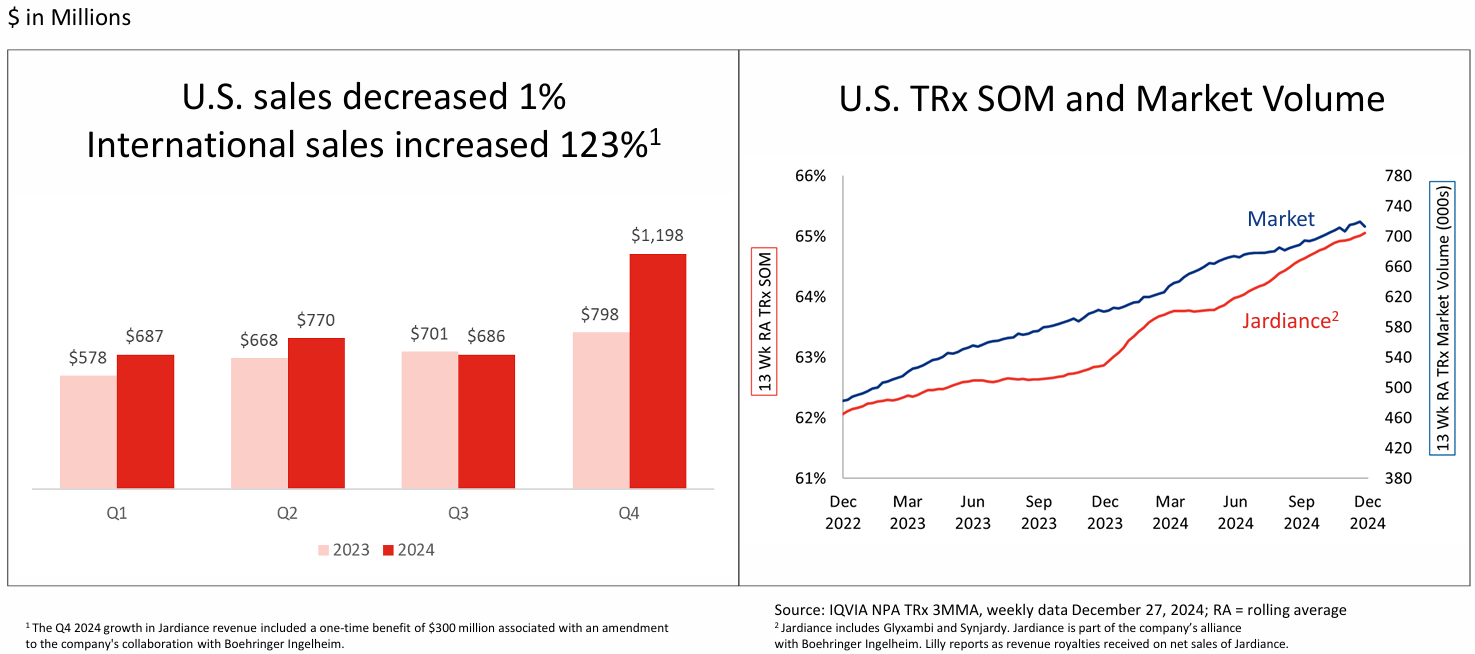

- Jardiance revenue and prescription trends (Source: Eli Lilly)

one-time benefit 제외하면 $900 mn 수준: 그래도 꽤 갑작스럽게 성장

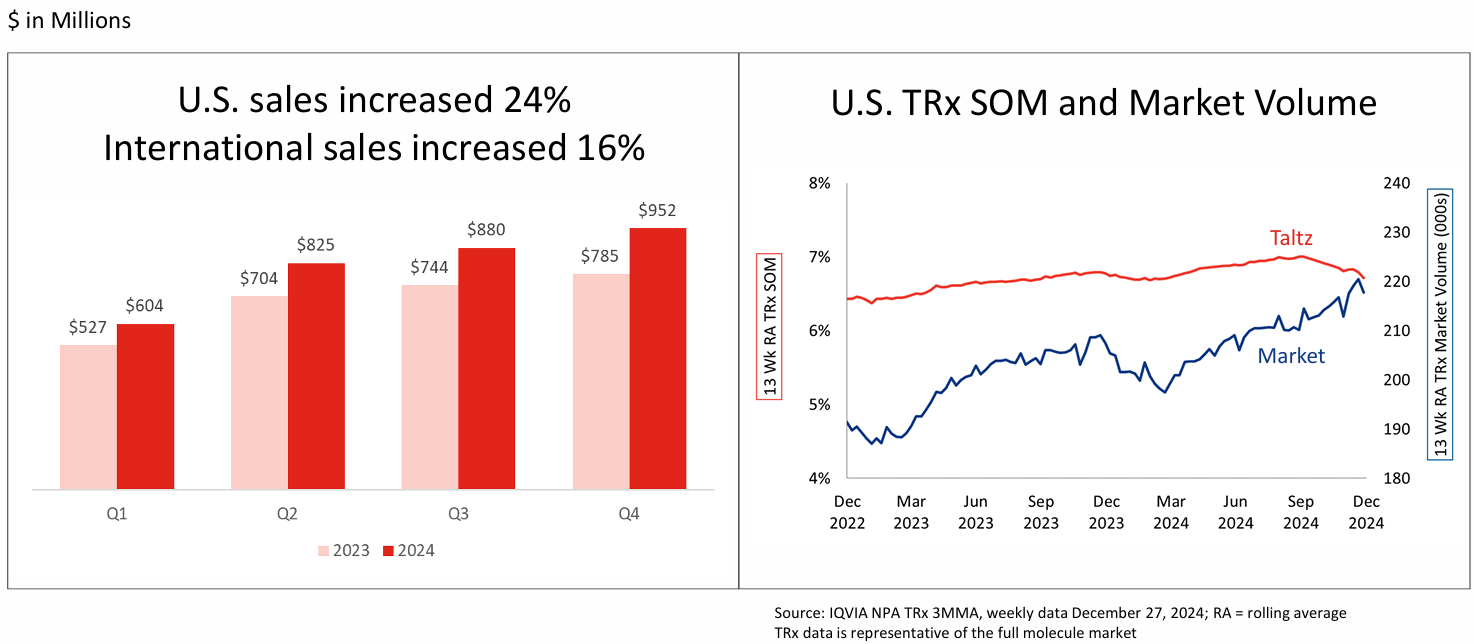

Taltz revenue and prescription trends (Source: Eli Lilly)

- Portfolio 쭉 둘러보면 non-incretin portfolio에서 실적을 방어해준 느낌이 강함

- 물론 incretin portfolio에 걸려있던 consensus 자체가 너무 높았던 영향도 있고

- 결국 4Q24 내내 consensus 하향하면서 최종적으로 earnings call에서는 slightly miss라는 결과를 받아들임

Q&A

Q. over the past 6 to 9 months, there has been a consistent cadence of data points questioning the size of the addressable and accessible obesity market, none of which are news, but include slowing prescription trends, Lilly meeting demand at least a year early, Lilly instituting DTC and extending co-pay cards despite struggling to meet demand, Lilly launching in OUS markets despite struggling to meet U.S. demand and significant stocking fluctuations and challenges in guiding. So taken collectively, these points are concerning. I think you will say that they all relate to the unprecedented size of the market and meeting its demand, but can you state that there has not been any conversations within Lilly questioning whether we are all significantly over our skis on this market and that the manufacturing build-out may simply be too aggressive?

I know why you’re asking it. And I think the perspective we have is that it’s early days on a very, very large opportunity. There’s turbulence. I’ll own that.

We always seek to put projections out that we can hit with confidence, but that are also within the range of possibilities. And in the back half of that year – last year, we fell short of that. But everything we’ve said is true, and we continue to believe in that this is a market with hundreds of millions of people globally that there is a unique thing here and that we can both prevent a large portion of chronic disease with obesity drugs.

Of course, as highlighting on this call, we’re getting close to, I think, a relief valve on that, which is the idea that you could have an oral which is scalable in a way that injectable systems just aren’t really test the question legitimately what is the edge of the demand curve. But we don’t think we’re close to it right now.

We’re still gating promotion and gating launches globally. That’s a different thing, and we’re building facilities as fast as we can to match up those 2 things, what we can make and what we can sell, and although we’re supplying the U.S. market well right now, we’ll need to do more, and I’m pretty confident in that. So hopefully, that gives you some color on the mindset here, and wouldn’t overread the turbulence and prediction challenges we have. But long term, we’re very bullish, and you’ll see us act according to that belief.

Q. So at JPMorgan, your team mentioned you expect GLP-1 pricing to be relatively stable in 2025. Are you implying that while you’ll give additional discounts to the channel to improve access, that will be offset by improved adherence? Or is it more Lilly’s reached a steady state on discounts at least until semaglutide gets put under IRA negotiation in 2026?

In terms of the pricing trends that I alluded during the JPMorgan conference and getting into 2025, first, we talk about the Q4. And into 2025, what we mentioned basically is a continuation of the trends. Remember that we had in the base period in 2023, an uncovered copay that basically created quite a lot of noise on the year-on-year comparison.

So we talk about basically adjusting by that, there is still single-digit erosion on our pricing trends, and that’s the same trends that I alluded that will continue into 2025

I think we have really good access on the Mounjaro side, over 90% in commercial and Part D, and I’ve already covered the commercial space for Zepbound. We expect access to continue to improve in 2025 as well.

Q. 지난 6-9개월 동안 비만 시장의 실제 규모와 접근 가능한 시장 규모에 대해 의문을 제기하는 데이터 포인트들이 지속적으로 나타났습니다. 처방 증가세 둔화, Lilly가 예상보다 최소 1년 일찍 수요를 충족한 점, 수요 충족에 어려움을 겪으면서도 DTC 광고를 시작하고 코페이 카드를 확대한 점, 미국 내 수요 충족에 어려움을 겪고 재고 변동이 크며 가이던스 제시에 어려움을 겪는 상황에서도 해외 시장에 진출한 점 등이 새로운 소식은 아니지만, 이러한 점들이 우려됩니다. 귀사는 이 모든 것이 전례 없는 시장 규모와 수요 충족과 관련이 있다고 말씀하시겠지만, Lilly 내부에서 우리 모두가 이 시장에 대해 너무 앞서나가고 있는 것은 아닌지, 제조 설비 확장이 단순히 너무 공격적인 것은 아닌지에 대한 논의가 전혀 없었다고 말씀하실 수 있습니까?

질문하시는 이유를 알겠습니다. 우리가 보는 관점은 매우 큰 기회의 초기 단계라는 것입니다. 불안정성이 있다는 점은 인정하겠습니다.

우리는 항상 자신 있게 달성할 수 있는 전망치를 제시하려고 노력합니다만, 그것도 가능성의 범위 내에서입니다. 작년 하반기에는 – 목표에 미치지 못했습니다. 하지만 우리가 말씀드린 모든 것이 사실입니다. 그리고 우리는 여전히 이것이 전 세계적으로 수억 명의 환자가 있는 시장이며, 여기에는 특별한 점이 있고, 비만 치료제로 만성 질환의 상당 부분을 예방할 수 있다고 믿고 있습니다.

물론 이번 컨퍼런스 콜에서 강조했듯이, 우리는 일종의 해결책에 가까워지고 있다고 생각합니다. 주사제 시스템과는 달리 확장성이 있는 경구용 약물을 개발할 수 있다는 아이디어인데, 이는 수요 곡선의 한계가 어디인지를 정당하게 시험해볼 수 있게 할 것입니다. 하지만 우리는 아직 그 수준에 가깝지 않다고 생각합니다.

우리는 여전히 프로모션과 글로벌 출시를 단계적으로 진행하고 있습니다. 이는 다른 문제이며, 우리가 만들 수 있는 것과 판매할 수 있는 것, 이 두 가지를 맞추기 위해 최대한 빠르게 시설을 건설하고 있습니다. 현재 미국 시장에 대한 공급은 잘 이루어지고 있지만, 더 많은 것이 필요할 것이고, 저는 그것에 대해 매우 확신하고 있습니다. 이것이 우리의 사고방식에 대한 통찰을 제공했기를 바랍니다. 현재의 불안정성과 예측의 어려움을 과대 해석하지 않으셨으면 합니다. 하지만 장기적으로 우리는 매우 낙관적이며, 여러분은 우리가 그 믿음에 따라 행동하는 것을 보게 될 것입니다.

Q. JPMorgan 컨퍼런스에서 귀사 팀은 2025년 GLP-1 가격이 비교적 안정적일 것으로 예상한다고 언급했습니다. 이는 접근성 개선을 위해 유통 채널에 추가 할인을 제공하더라도 복약 순응도 개선으로 상쇄될 것이라는 의미입니까? 아니면 세마글루타이드가 2026년 IRA 협상 대상이 되기 전까지 Lilly의 할인이 안정 상태에 도달했다는 의미입니까?

JPMorgan 컨퍼런스에서 언급했던 가격 동향과 2025년 전망에 대해 말씀드리자면, 먼저 4분기에 대해 이야기하겠습니다. 2025년에 대해서는 기본적으로 현재 추세가 지속될 것이라고 말씀드렸습니다. 2023년 기준 기간에 보험 미적용 코페이가 있었고, 이로 인해 전년 대비 비교에 상당한 노이즈가 발생했다는 점을 기억해주시기 바랍니다.

이를 감안하더라도 우리의 가격 동향에는 여전히 한 자릿수 하락이 있습니다. 그리고 이러한 추세는 2025년에도 계속될 것이라고 말씀드렸습니다.

Mounjaro는 상업보험과 파트 D에서 90% 이상의 매우 좋은 접근성을 확보하고 있으며, Zepbound의 상업보험 부문에 대해서도 이미 말씀드렸습니다. 2025년에도 접근성이 계속 개선될 것으로 예상합니다.

- 4Q24 earnings call (Source: Eli Lilly)

- Q&A에서는 이 두 개의 질의응답이 사실상 핵심이었음

- Guidance miss한 것에 대한 사과를 사실상 했음

- 그리고 2025년에도 single-digit price erosion이 있을 것이라고 함

- 더 이상 GLP-1에 관심갖지 않아도 될 것 같다

- 비만약이 세상을 바꾸는 thesis는 실현되지 않을 가능성이 높음, 최소한 증설이 다 끝나는 순간까지는

- 일단 약이 지나치게 비싸서 mass public으로 널리 활용되는 것 자체가 불가능한 수준

- 이 약을 만드는 회사에 투자하는 입장에서는 가격과 상관없이 (정확하게는 가격이 비쌈에도 불구하고) 많이 팔려서 모두가 맞으면서 인류가 건강해질거야라는 narrative가 전개됐던 때를 비교해보면

- 정작 약을 정말 싸게 팔면서 인류 전체의 건강을 증진하게 되는 narrative는 전혀 다른 역학으로 분석해야 하는 상황이다

- Valuation challenge에서 작성했던 글을 다시 회수하고 싶은 심정이긴 한데…

- 마침내 입사부터 지금까지 나를 괴롭혀(?)왔던 pharmaceuticals 섹턴와의 결별

Disclaimer!

- 본 게시물은 단순 의견 및 기록 목적으로 작성되었으며 특정 투자상품의 매수·매도·보유 등 투자 권유를 의미하지 않습니다

- 본 게시물은 작성자 개인의 판단에 근거하여 작성되었고, 작성자 본인이 속한 기관의 의견을 대변하지 않습니다

- 본 게시물은 작성자 본인이 작성일 시점에 신뢰할 만하다고 판단하는 자료와 정보에 근거하였으나, 정확성이나 완전성, 신뢰성을 보장하지 않습니다

- 본 게시물은 그 어떠한 경우에도 증권, 파생상품 등 금융투자상품에 대한 투자조언으로 해석될 수 없습니다

- 본 게시물은 투자자의 투자 결과에 대해 어떠한 목적의 증빙자료로도 사용될 수 없습니다

- 본 게시물을 이용함으로써 발생하는 직·간접적 손실에 대해 어떠한 책임도 지지 않습니다