- https://www.bloomberg.com/news/features/2025-03-16/wall-street-s-dark-pools-grow-murkier-with-private-rooms

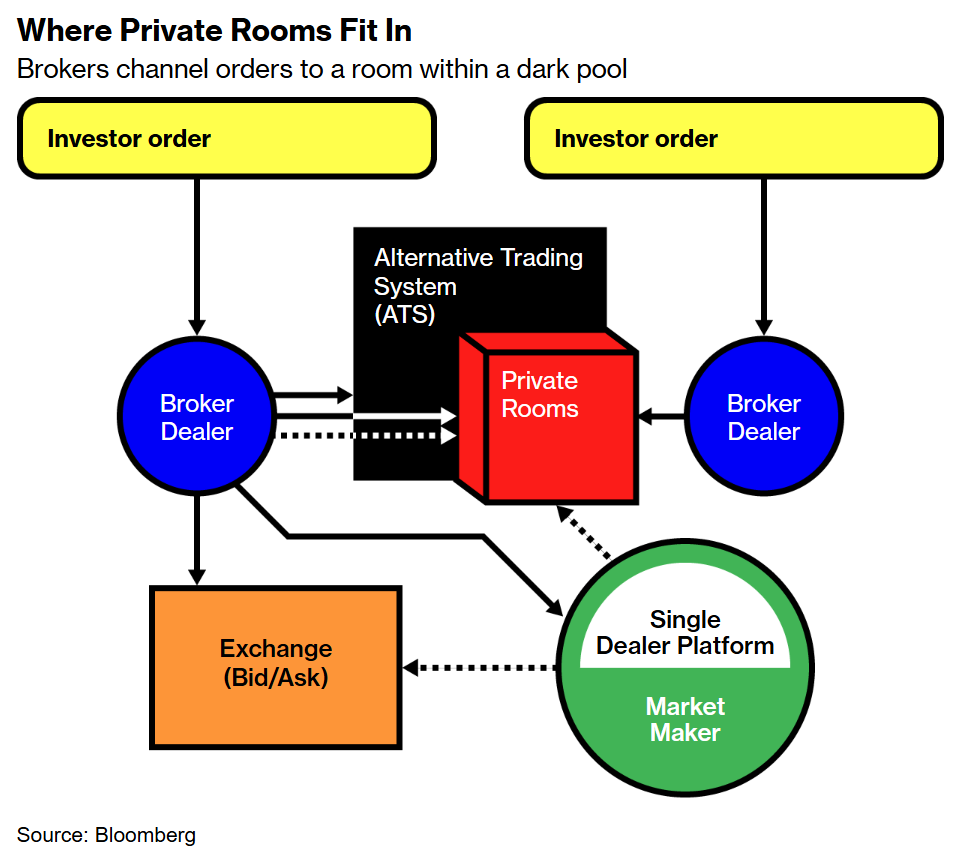

They’re offering what are dubbed private rooms, gated venues that take the core benefit of a dark pool — the ability to hide big equity deals so they won’t impact prices — and add exclusivity, specifying exactly who can partake in any trade.

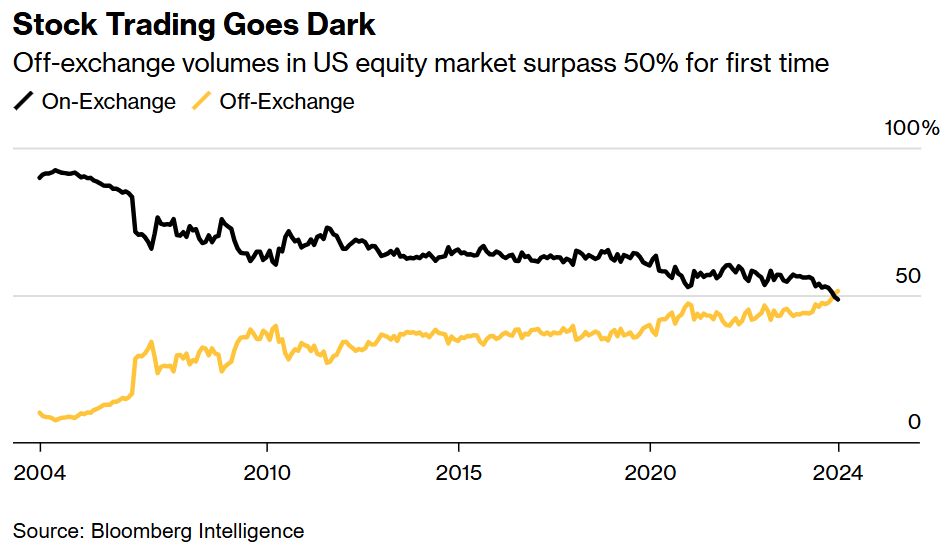

Created within the dark pools themselves, the rooms are independent from one another and each is invisible to anyone not invited, raising questions about both market transparency and fragmentation. But with more than half of all US stock trading now happening away from public exchanges, they’re in high demand from firms eager to choose whom they do business with, often to help them carry out individual orders more efficiently.

Right now, it’s impossible to say how many private rooms exist, or how much activity is moving through them. Companies operating alternative trading systems, or ATS — the formal term for dark pools — say it’s a minority of their volumes at present, since the growth in demand is a relatively new phenomenon.

이들은 ’프라이빗 룸(private rooms)’이라 불리는 공간을 제공하고 있습니다. 이는 폐쇄된 거래 장소로, 다크풀(dark pool)의 핵심 장점인 대규모 주식 거래를 숨겨 가격에 영향을 미치지 않도록 하는 기능을 유지하면서도, 참가자를 엄격히 지정하여 배타성을 더한 개념입니다.

이러한 프라이빗 룸은 다크풀 내부에서 생성되며, 각각 독립적으로 운영되며 초대받지 않은 사람에게는 완전히 보이지 않습니다. 이로 인해 시장의 투명성과 단편화(fragmentation)에 대한 우려가 제기되고 있습니다. 그러나 현재 미국 주식 거래의 절반 이상이 공공 거래소가 아닌 곳에서 이루어지고 있으며, 기업들은 거래 상대를 선택할 수 있는 옵션을 선호하고 있어 이러한 프라이빗 룸에 대한 수요가 높아지고 있습니다. 이는 주로 개별 주문을 보다 효율적으로 처리하는 데 도움이 되기 때문입니다.

현재 프라이빗 룸이 정확히 몇 개 존재하는지, 혹은 이들 통해 얼마나 많은 거래가 이루어지는지는 알 수 없습니다. 다크풀의 공식 용어인 대체거래시스템(ATS, Alternative Trading Systems)을 운영하는 기업들은 아직 이러한 룸이 전체 거래량에서 차지하는 비중이 적다고 말합니다. 이는 프라이빗 룸에 대한 수요 증가가 비교적 최근에 나타난 현상이기 때문입니다.

Dark pools are so-called because the trades they handle happen away from the “lit” public exchange. That helps prevent order details leaking to the broader market and triggering adverse price moves before they can be executed. But there’s still a downside: a pool is open to anyone, and firms inside never know who their counterparty is in any trade. Private rooms can be even more discreet.

다크풀은 ‘어둠(dark)’이라는 이름처럼 거래가 ‘밝은(lit)’ 공공 거래소에서 이루어지지 않기 때문에 이렇게 불립니다. 이를 통해 주문 정보가 시장에 노출되는 것을 방지하고, 거래 실행 전에 불리한 가격 변동이 발생하는 것을 막을 수 있습니다. 그러나 다크풀의 단점은 모든 참가자가 누구와 거래하는지 알 수 없다는 점입니다. 반면, 프라이빗 룸은 더욱 높은 수준의 비밀 유지가 가능합니다.

Execution excellence

Private rooms are known by a slew of other names including hosted pools, restricted-access rooms, ATS pools, and custom counterparty groups. They’re gaining popularity in the huge, ultra-fast modern market as a way to help firms avoid losing out against players who may be able to move quicker or who have access to superior information.

Private rooms are known by a slew of other names including hosted pools, restricted-access rooms, ATS pools, and custom counterparty groups. They’re gaining popularity in the huge, ultra-fast modern market as a way to help firms avoid losing out against players who may be able to move quicker or who have access to superior information.

“The problem we have is, how do we identify good versus bad liquidity?” says Jatin Suryawanshi, global head of quant strategy at Jefferies, who estimates that 15 in every 100 shares executed by the firm’s algorithms currently move via a room. “In using private rooms, you can prioritize who you want to interact with.”

프라이빗 룸은 호스티드 풀(hosted pools), 제한 접근 룸(restricted-access rooms), ATS 풀(ATS pools), 맞춤형 거래상대 그룹(custom counterparty groups) 등 다양한 이름으로 알려져 있습니다. 초고속으로 진행되는 현대 금융 시장에서 이러한 룸은 더욱 인기를 얻고 있으며, 기업들이 더 빠르게 움직이거나 우월한 정보를 보유한 거래자들과 경쟁하는 과정에서 손실을 피하는 방법으로 활용되고 있습니다.

프라이빗 룸은 호스티드 풀(hosted pools), 제한 접근 룸(restricted-access rooms), ATS 풀(ATS pools), 맞춤형 거래상대 그룹(custom counterparty groups) 등 다양한 이름으로 알려져 있습니다. 초고속으로 진행되는 현대 금융 시장에서 이러한 룸은 더욱 인기를 얻고 있으며, 기업들이 더 빠르게 움직이거나 우월한 정보를 보유한 거래자들과 경쟁하는 과정에서 손실을 피하는 방법으로 활용되고 있습니다.

“우리가 직면한 문제는 ’좋은 유동성’과 ’나쁜 유동성’을 어떻게 구별하느냐는 것입니다.”라고 제프리스(Jefferies)의 글로벌 퀀트 전략 책임자인 자틴 수리야완시(Jatin Suryawanshi)는 말합니다. 그는 현재 회사의 알고리즘을 통해 실행되는 주식 100주당 약 15주가 프라이빗 룸을 통해 거래되고 있다고 추정합니다. “프라이빗 룸을 사용하면 누구와 거래할지 우선순위를 정할 수 있습니다.”

Private room growth has accelerated amid the migration of stock trading away from public exchanges and as their use has become more common. They emerged at the ATS firm LeveL as far back as 18 years ago. LeveL started by allowing firms to match their own orders, in what’s known as internalization. That expanded to other forms of segmentation, including bi-lateral and multi-lateral agreements, where one party agrees to trade with another, or multiple parties agree to only interact with each other, within the same ATS.

Private rooms are not generally needed by big banks or brokers who have the resources to create their own ATS or what are called single-dealer platforms. That’s another breed of off-exchange trading venue where the operator is always the counterparty to any trade.

But for smaller players, it’s too expensive and cumbersome to build and manage an ATS or SDP, meet the associated regulatory reporting requirements and set up the necessary connections. Arranging a private room at an established ATS is a solution.

프라이빗 룸의 성장 속도는 주식 거래가 공공 거래소에서 벗어나면서 더욱 가속화되었으며, 그 사용도 점점 일반화되고 있습니다. 이러한 룸은 18년 전 ATS(대체거래시스템) 기업인 LeveL에서 처음 등장했습니다. LeveL은 기업들이 자체 주문을 매칭할 수 있도록 하는 내부화(internalization) 개념으로 시작되었으며, 이후 양자(bi-lateral) 및 다자(multi-lateral) 계약과 같은 다양한 형태의 세분화로 확대되었습니다. 이 방식에서는 한 당사자가 특정 상대와만 거래하기로 하거나, 여러 당사자가 같은 ATS 내에서 서로만 거래하기로 합의하는 구조를 갖습니다.

프라이빗 룸은 일반적으로 대형 은행이나 브로커들에게는 필요하지 않습니다. 이들은 자체 ATS 또는 싱글 딜러 플랫폼(SDP, Single-Dealer Platform)을 구축할 수 있는 자원을 보유하고 있기 때문입니다. SDP는 또 다른 형태의 장외(off-exchange) 거래소로, 운영자가 모든 거래의 상대방이 되는 시스템입니다.

그러나 중소 규모 기업들에게는 ATS나 SDP를 구축하고 운영하는 것이 비용적으로 부담스럽고 복잡한 과정입니다. 또한, 관련 규제 보고 의무를 준수하고 필요한 연결망을 설정하는 것도 쉽지 않습니다. 따라서 기존 ATS에서 프라이빗 룸을 마련하는 것이 현실적인 해결책이 됩니다.

At IntelligentCross, the majority of rooms currently offered serve institutional brokers that don’t have capacity to conduct similar activities internally. Jefferies trades in a private room provided by the firm where it interacts with seven other brokers who don’t have their own ATS, but have institutional orders, according to Suryawanshi.

IntelligentCross에서는 현재 제공되는 프라이빗 룸의 대부분이 자체적으로 이러한 활동을 수행할 능력이 없는 기관 브로커들을 위한 것입니다. 제프리스(Jefferies)는 이 회사에서 제공하는 프라이빗 룸에서 거래를 수행하며, 자체 ATS는 없지만 기관 주문을 보유한 7개의 다른 브로커들과 상호 작용한다고 수리야완시(Suryawanshi)는 설명합니다.

Dark disclosure

Not every ATS is rushing to embrace private rooms. New York-based PureStream offers “pools” that operate like rooms, but they are disclosed to all subscribers if they are created, and anyone can join. In essence, the room is open to all.

Perhaps the biggest criticism of private rooms is that they create phantom liquidity, because transactions taking place inside a room are simply lumped in with the total activity reported by its dark pool parent. That creates a misleading picture for anyone trying to gauge market depth, since reported trading volumes include activity not available to those outside the room.

ATS are regulated trading venues, overseen by the Securities and Exchange Commission, which in 2018 enhanced its supervision of such venues by imposing new disclosure requirements. Each dark pool must now file a form, ATS-N, which gives an overview about the specific trading mechanisms on its platform.

“There are no rules to force ATS to break out the identity of single-dealer rooms or their volume,” Larry Tabb, head of market structure at Bloomberg Intelligence, wrote in a May note. The Financial Industry Regulatory Authority “does a good job of ATS volume reporting on a post-execution basis. Yet there are no rules to aid analysts or users looking to break down the percentage of ATS volume executed in the open pool vs. the private room, or the volume executed using segmentation strategies,” he wrote.

Dark pools are no strangers to transparency worries. Their opacity provoked extensive media coverage and regulatory scrutiny about a decade ago amid speculation they gave high-frequency firms advantages against other investors — attention partly prompted by the bestselling book Flash Boys.

모든 ATS가 프라이빗 룸을 적극적으로 도입하는 것은 아닙니다. 뉴욕에 본사를 둔 PureStream은 프라이빗 룸과 유사하게 작동하는 “풀(pools)”을 제공하지만, 생성될 경우 모든 가입자에게 공개되며, 누구나 참여할 수 있습니다. 본질적으로 이 룸은 개방형(open) 구조입니다.

프라이빗 룸에 대한 가장 큰 비판 중 하나는 유령 유동성(phantom liquidity)을 초래한다는 점입니다. 프라이빗 룸 내부에서 이루어진 거래는 해당 다크풀의 전체 거래량에 포함되어 보고되지만, 룸 외부에서는 이를 확인할 수 없습니다. 이로 인해 시장의 유동성을 평가하려는 투자자들에게 왜곡된 정보를 제공할 수 있습니다.

ATS는 미국 증권거래위원회(SEC)의 규제를 받는 거래소이며, 2018년 SEC는 이러한 플랫폼에 대한 감독을 강화하면서 새로운 공시 요건을 부과했습니다. 이에 따라 각 다크풀은 거래 메커니즘에 대한 개요를 제공하는 ATS-N 양식을 제출해야 합니다.

블룸버그 인텔리전스(Bloomberg Intelligence)의 시장 구조 책임자인 래리 태브(Larry Tabb)는 지난 5월 보고서에서 “ATS가 싱글 딜러 룸의 정체성이나 거래량을 별도로 공개하도록 강제하는 규정이 없다”고 지적했습니다. 또한 금융산업규제당국(FINRA)는 “거래 체결 후 ATS의 거래량 보고를 효과적으로 수행하고 있지만, 분석가나 투자자들이 ATS에서 개방형 풀과 프라이빗 룸 간의 거래 비율을 분석하거나, 세분화된 거래 전략을 통해 집행된 거래량을 구분하는 것을 돕는 규정은 존재하지 않는다”고 덧붙였습니다.

다크풀은 투명성 논란이 새로운 것이 아닙니다. 약 10년 전, 다크풀이 고빈도 거래(high-frequency trading) 업체들에게 다른 투자자들보다 유리한 환경을 제공한다는 의혹이 제기되면서 언론과 규제 기관의 집중적인 감시를 받았습니다. 이러한 관심은 부분적으로 베스트셀러 도서 《플래시 보이즈(Flash Boys)》의 영향으로 촉발되었습니다.

‘Growth mode’

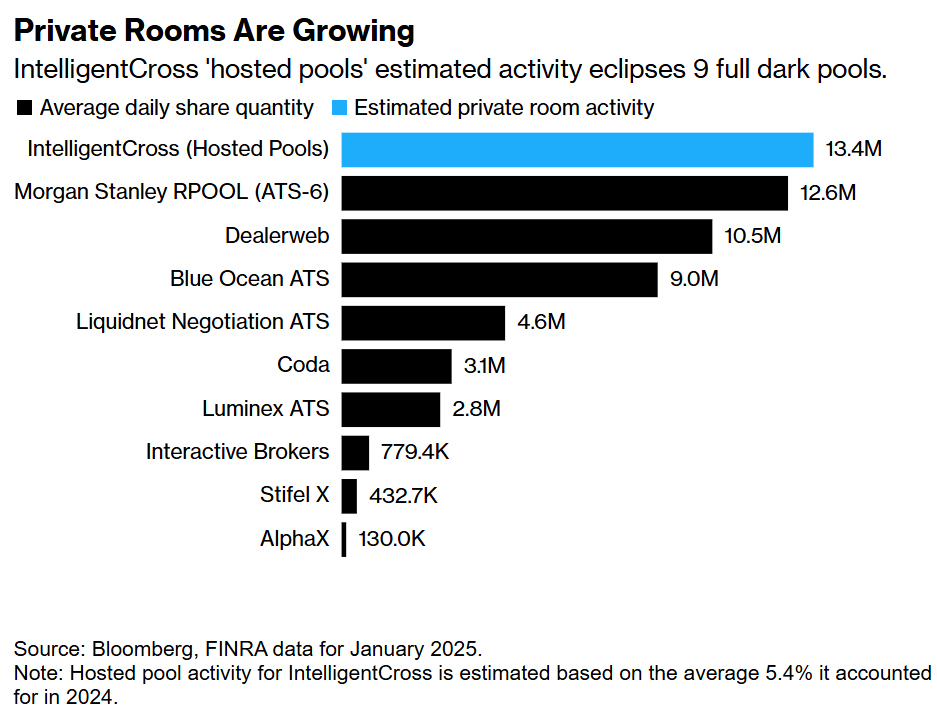

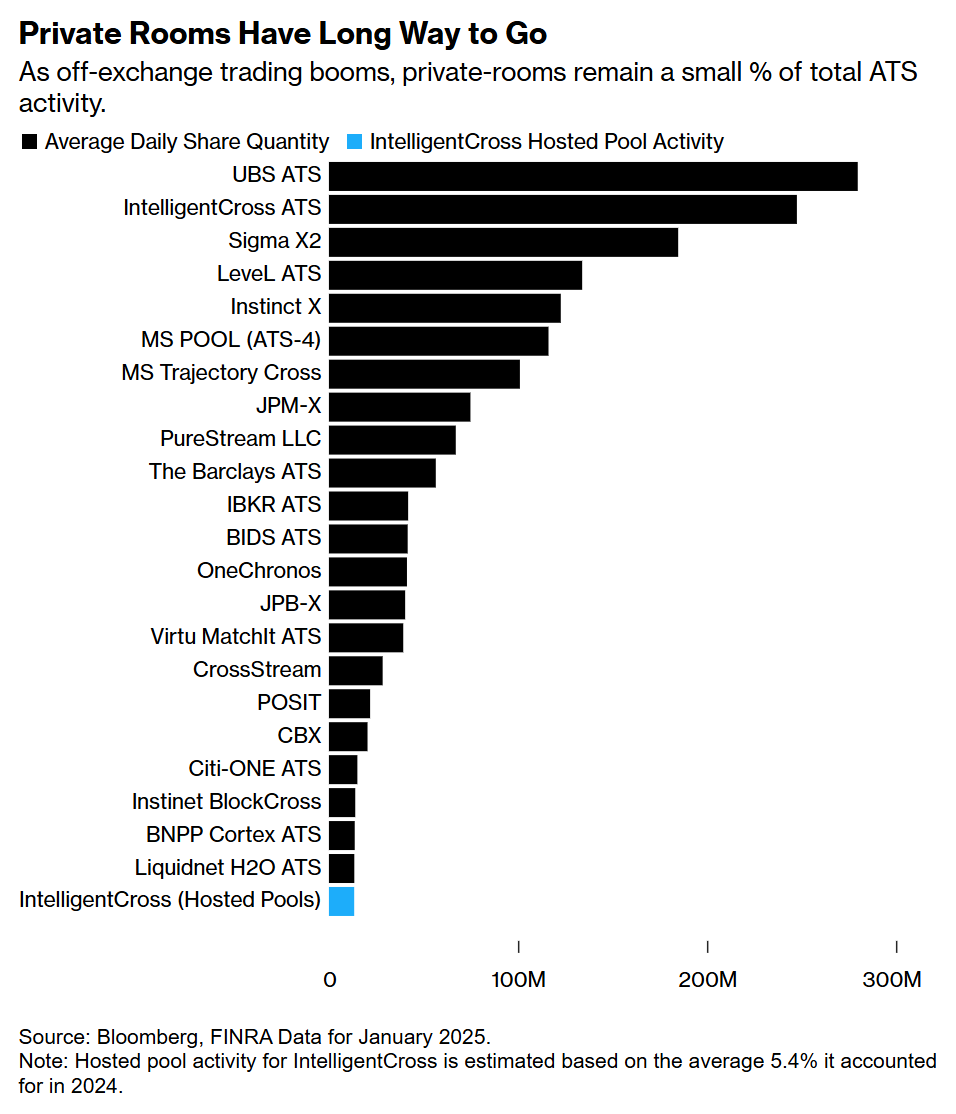

For their users, private rooms are a handy tool, but still one of a set. Hosted pools represent a single-digit percentage of IntelligentCross’s overall volumes for now — an average of about 5.4% last year — because they’re so new, according to Ginis. “It will take brokers some time to optimize for this,” he says.

프라이빗 룸을 이용하는 기업들에게 이는 유용한 도구이지만, 전체적인 거래 전략의 일부에 불과합니다. IntelligentCross의 대표 기니스(Ginis)에 따르면, 현재 호스티드 풀(hosted pools)은 회사 전체 거래량의 한 자리 수 비율을 차지하며, 지난해 평균 5.4% 정도였습니다. 그는 “이 기능이 아직 새롭기 때문에 브로커들이 최적화하는 데 시간이 걸릴 것”이라고 말합니다.

“Many firms are setting up private rooms these days,” says Gurliacci, who used to work for the NYSE. “They are innovative, and here to stay. There is more going on there than most people know.”

과거 뉴욕증권거래소(NYSE)에서 근무했던 굴리아치(Gurliacci)는 “요즘 많은 기업들이 프라이빗 룸을 구축하고 있다”며, “이는 혁신적인 방식이며, 앞으로도 지속될 것이다. 대부분의 사람들이 알고 있는 것보다 훨씬 더 많은 일이 이 안에서 벌어지고 있다”고 강조했습니다.